Snow damage can raise serious questions for Wisconsin homeowners. Heavy accumulation, ice buildup, and rapid freeze–thaw cycles place stress on roofs, gutters, and structural components throughout the winter. When damage occurs, many homeowners assume their policy will cover the repairs. In reality, the answer depends on how the damage happened and how the insurance policy applies to that specific situation.

Many homeowners ask the same question after a major winter storm: does homeowners insurance cover snow damage, or will my insurer deny the claim? A standard home insurance policy may provide coverage for certain types of winter storm damage, but whether homeowners insurance coverage applies depends on the specific policy, the cause of the loss, and the exclusions listed in the home insurance policy.

At Wallace Law, we regularly speak with homeowners who are unsure whether their winter property damage should be covered. Most home insurance policies may provide coverage when winter weather causes sudden and accidental damage, but insurers sometimes argue that the loss resulted from structural deterioration, poor maintenance, or other homeowners insurance exclusions. Understanding how coverage works can help you respond more effectively if damage occurs.

What Types of Snow Damage Are Typically Covered?

Homeowners insurance generally covers sudden and accidental damage caused by a covered peril. When heavy snow or winter storms directly cause structural damage, the loss may fall within homeowners insurance coverage.

Several types of snow related damage are often covered when they result from a sudden winter event.

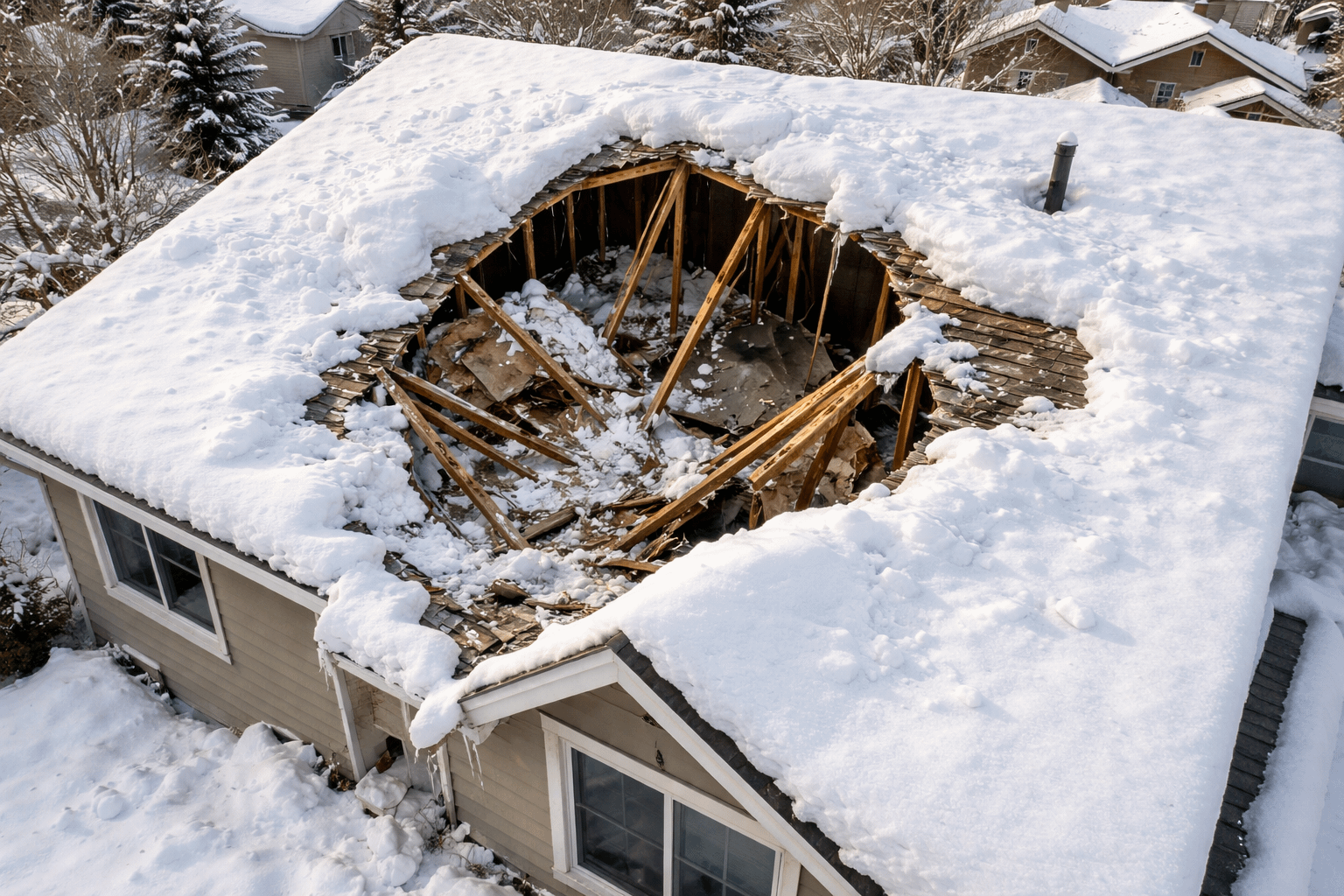

Roof Collapse From Snow Load

One of the most serious winter claims involves roof collapse caused by the weight of heavy snow. In Wisconsin, prolonged storms can produce dense snow that places extraordinary pressure on roofing systems.

During severe winter weather, the weight of accumulated snow and ice may cause structural failure. When a roof collapse snow insurance claim arises from a sudden accumulation, most home insurance policies may provide coverage for the structural damage and resulting damage inside the home.

However, insurance companies frequently examine these claims closely. An insurance company may argue that the collapse resulted from long-term deterioration, improper construction, or poor maintenance rather than the weight of snow alone.

Ice Dams and Interior Water Damage

Ice dams are another common source of snow damage in Wisconsin. They form when heat escaping from the home causes melting snow on the roof. The water then refreezes along the roof edge, creating ice buildup that prevents proper drainage.

When this occurs, snow and ice can force water beneath shingles and into the home. This type of intrusion may lead to water damage, damaged insulation, and ceiling stains.

Interior damage from ice dams may affect:

- Drywall and ceilings

- Flooring and insulation

- Stored personal property and other personal belongings

Many policies may cover the resulting damage to the interior of the home even if the ice dam itself is not specifically covered.

Snow Impact and Structural Stress

Accumulating snow and ice can also cause damage through structural stress or physical impact.

Large sheets of ice sliding from a roof may damage gutters, decks, or exterior structures. In some situations, falling objects such as a tree or branch weighed down by snow may strike the roof or other parts of the house, creating serious damage.

In Wisconsin, storm damage during winter often combines several factors at once. Storm damage may involve both snow damage and wind damage, which can complicate how the insurance provider evaluates the claim.

Frozen Pipes Related to Snow Conditions

Another winter issue involves frozen pipes. Extended periods of frigid temperatures combined with heavy snowfall can cause plumbing systems to freeze.

If pipes freeze and burst despite reasonable precautions, many home insurance policies may provide coverage for the resulting water damage and necessary repairs. Insurers often investigate whether homeowners took steps to protect the property, such as maintaining heat or taking steps to insulate pipes during extreme cold.

What to Do If Snow Damages Your Roof

When snow damage affects a roof or structure, the steps taken immediately afterward can influence the outcome of the insurance claim.

The first priority is safety and preventing additional damage caused by continued accumulation or water intrusion. After conditions are safe, homeowners should focus on documentation.

Important steps include:

- Photographing visible snow damage and snow accumulation

- Documenting the date of the winter storm or winter weather event

- Saving contractor estimates and inspection reports

- Preserving damaged materials for the insurance company inspection

- Reporting the snow damage insurance claim to the insurance provider promptly

Thorough documentation helps establish the timeline of the loss. When insurers evaluate a snow damage insurance claim, they often rely on inspection reports and weather records to determine whether the damage occurred during a specific storm.

Why Insurance Companies Deny Snow Damage Claims

A denied snow damage claim usually centers on the cause of the damage rather than the presence of snow itself.

Insurance companies frequently argue that the damage resulted from preexisting conditions instead of a sudden winter storm. A typical insurance company explanation may include claims that the roof was aging, the structure weakened over time, or that poor maintenance contributed to the loss.

Common reasons insurers deny roof damage claims include:

- Wear and tear or aging roofing materials

- Structural deterioration over time

- Improper installation or construction defects

- Gradual water damage rather than sudden storm loss

Under Wisconsin law, insurers must investigate claims reasonably and evaluate them in good faith. When an insurance company relies on a homeowners insurance exclusion, it must be able to support that position with evidence gathered during the investigation.

The cause of the loss often becomes the central dispute in a denied snow damage claim.

Your Fight Ends Here

Schedule a Free Legal Consultation

Homeowners Insurance Exclusions That Affect Snow Damage Claims

Every insurance policy contains exclusions that limit coverage in certain situations. These homeowners insurance exclusions often play a major role when insurers review snow damage claims.

Common exclusions cited by insurance providers include:

- Wear and tear or deterioration

- Construction defects

- Long-term moisture exposure

- Lack of maintenance

Although these exclusions exist, they must be applied correctly. The presence of aging materials does not automatically mean that snow damage was not a contributing cause.

Determining whether coverage applies requires careful review of the specific policy language and the facts surrounding the loss. If you’re facing an insurance dispute or denial, call Wallace Law so we can review your policy and explain your options.

Wisconsin Law and the One-Year Deadline for Insurance Claims

Another issue many homeowners do not expect involves the time limit for challenging an insurance company decision.

In Wisconsin, many home insurance policies contain a clause requiring lawsuits against the insurance company to be filed within one year from the date of loss. This shortened deadline is permitted under state law and appears in many insurance policies.

The one-year period usually begins on the date the snow damage occurred, not when the claim is denied. Ongoing discussions with the insurance provider do not automatically extend that deadline.

For homeowners dealing with major property damage, understanding this deadline can be critical.

How a Wisconsin Insurance Lawyer Can Help

When snow damage claims are disputed, the issue usually involves how the insurance company interprets the insurance policy and applies exclusions.

At Wallace Law, we review the insurance policy, evaluate inspection findings, and analyze whether the insurance provider properly investigated the claim. This includes examining whether the insurer accurately determined the cause of the snow damage and whether the policy exclusions were applied correctly.

Our work often involves reviewing engineering reports, assessing the extent of structural damage, and determining whether the coverage options available under the policy were properly considered.

Early review of the claim can also help ensure that homeowners do not miss the one-year deadline for filing suit under Wisconsin insurance law.

Snow Damage Claim Denied? Contact Wallace Law

Snow damage can cause significant damage to a home, but disputes with an insurance company are common. Insurers frequently argue that the damage resulted from deterioration, structural weakness, or other exclusions rather than a winter storm.

At Wallace Law, we represent homeowners facing insurance disputes involving winter storm damage, roof collapse, and other snow related damage. If your claim has been denied or undervalued, we can review the circumstances and explain the options available under Wisconsin law. Call or contact us today.