Insurance — and the protection it offers us — is one of the first concerns we deal with after a crisis of some kind. Insurance policies are there to safeguard us when a loved one dies, a medical emergency occurs, or a tornado damages your home.

The over-arching theory is relatively simple but the details become complex. Insurance is financial protection for the unexpected, and a claim is how you get paid to recover your losses. Naturally, policyholders want to know how they should get paid, how much, and when they should receive the money from their insurer.

The claim processing procedure varies from insurer to insurer. Beyond that, every state also has guidelines to ensure insurance companies pay claims in a reasonable time frame without unnecessary delays. Unfortunately, not all claims get paid or paid on time: Some insurance companies follow the rules, while others refuse, reject, and stall payments intentionally.

Continue reading for more on how claims are processed, what to expect, and how to navigate claim delays with legal solutions.

What Is an Insurance Claim?

Insurance is a financial agreement between a policyholder and an insurance company.

What Does Filing a Claim Mean?

Many policies require a claim to issue a payout to the policyholder. An insurance claim is a formal request by a policyholder asking their insurance company for reimbursement to cover losses and expenses following an eligible accident, injury, or incident.

How Do Insurance Claims Work?

Most claims follow the same process — insurers validate the claim submission, review supporting documentation, facilitate an investigation, and make a decision that results in approval, denial, or rejection. Sometimes, claims result in quick payouts; other times, specific roadblocks or bad faith insurers stall claims deliberately.

Insurance policies that usually require claims include travel, life, health, and property insurance. Examples of incidents might consist of hospital stays, travel delays or cancellations, property damage, or theft.

What Are the Different Types of Insurance Claims?

Insurers pay out claims when an unexpected covered event occurs, and the policyholder needs to recover their losses.

Travel: Travel-related mishaps, like flight cancellations, illnesses, or missing luggage, are common. Travel claims happen when insurers fail to pay for a policyholder’s losses despite their coverage.

Health: Health insurance allows for necessary access to medical care, but denied claims can often stand in the way. Claims you should be covered for might be denied and cause inconvenient out-of-pocket costs.

Life: Funds from life insurance help with urgent costs like funeral arrangements, living expenses, and more. When insurers stall a life insurance payout, they put beneficiaries’ in a compromising financial position.

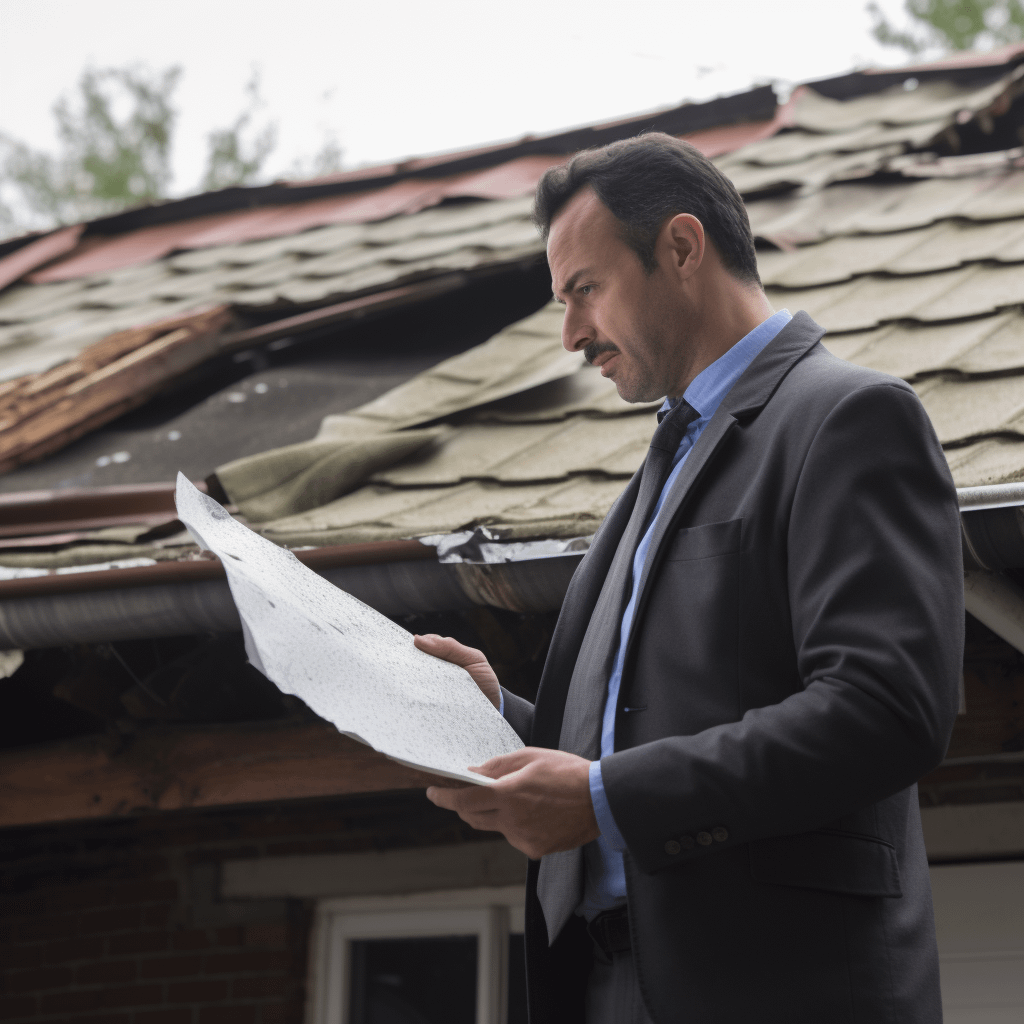

Property: Natural disasters can wreak havoc on a person’s home, requiring months or years of repair and rehab. Home insurance is supposed to offer financial support for an unexpected event. Still, it is common to experience claim denialsand payment settlements that are lower than the claim is worth.

Commercial property: Commercial properties are not immune to property theft and natural disasters. A claim payout ensures owners can avoid shutdowns or other disruptions to their business — unless an insurer intentionally denies a claim.

Bad faith: Some insurers use unethical strategies to deny and stall claims so they do not have to pay policyholders. This is an area Wallace Law specializes in. We help people recover significant losses when an insurer fails to meet the obligations of their contract.

How Is Damage Assessed During a Claim?

Damage assessments depend on the insurance policy and state laws. Using the Wisconsin property insurance claims process as an example, property owners must complete a proof of loss form and include detailed evidence of damages, such as photos, to ensure a speedier claims resolution. Policyholders must begin the bidding process with contractors to get repairs started.

A policy might indicate replacement value, which is the amount of money it would take to completely replace the structure of your home. A property must be insured to at least 80 percent of its replacement value to collect the total amount on a partial loss.

Alternatively, if your policy pays actual cash value, the insurance company is committing to pay the cost to repair or rebuild your house, excluding depreciation. The insurance company could use a variety of metrics to determine depreciation. You might only expect to be paid for part of the repairs.

In another scenario, recoverable depreciation is the difference between actual cash value and replacement cost. This clause in the insurance policy allows the homeowner to claim the difference.

As an example of how depreciation is calculated:

- A homeowner buys a $2,000 stove.

- The stove has held its value for ten years.

- To get to the depreciated amount, an insurance company looks at the following: $2,000 / 10 = $200 per year.

How Do Insurance Companies Send Money To You?

Insurance policies usually include verbiage regarding how claim payments are handled in the fine print. This includes whether money is distributed via insurance check, direct deposit, or distributed to a third party on your behalf.

1. Check: Some insurance companies issue claim payments by check. It is possible to receive multiple settlement checks at staggered times until a claim is satisfied.

2. Direct Deposit: Your insurer might request direct deposit information upfront if you submit a claim. You might receive a letter or email notification that funds are being deposited in your account following a claim approval.

3. Paying another party (like a mechanic or mortgage lender) directly: Some insurance companies pay third parties directly. For example, this might apply after a natural disaster hits your home and you need immediate repairs. During the homeowners insurance claim process, your insurance company might pay the contractor directly out of your claim.

If there are any questions or doubts regarding your insurer’s claim policies and payment distribution methods, consider getting legal advice from an experienced insurance dispute lawyer to rule out any concerns.

How Do Insurance Claims Get Paid?

The claims payout process is often staggered; most policyholders receive multiple checks. Sometimes, policyholders can keep the leftover money, but only occasionally.

In most cases, policyholders receive an advance against the total settlement as a first installment, followed by one or more payments until the claim has been satisfied and the claims payout process has closed.

With any payout, there are always terms to consider. For instance, if a policyholder cashes a check, there might be fine print stating that they cannot contest the payout later or take legal action.

In the property damage insurance claims process, a policyholder might get replacement value for their items, but they might be responsible for financially replacing them. You typically do not have direct control of the payment. Your insurance company might have to pay a contractor directly, or your lender or management company might have that control.

Insurance Claim Timing Guidelines

The state you live in dictates how much time you have to file and settle a claim, in addition to guidelines from the insurance company.

How Long Do I Have to File a Claim and Get Paid

The different types of insurance claims, such as health and life, travel, or property insurance, have different filing requirements depending on the insurer and state. Generally speaking, many policies require that claims are filed within 90 days to one year of the loss or event.

How to Speed Up the Insurance Claims Process

The quickest way to get your claim approved and paid is by doing your due diligence. It is important to comply with the insurance company’s claims submission process, which includes reviewing the fine print of your policy regarding coverage, providing thorough documentation, filling out the necessary paperwork, and meeting the insurer’s deadlines.

If the insurer denies your claim, this can extend the processing timeline and stall a payout. In this case, you can consult an experienced insurance dispute lawyer to understand your rights and options, including an appeal or other alternatives.

Your Fight Ends Here

Schedule Your Free Legal Consultation

What Can Delay My Claim Payment

Claims get denied for many reasons, depending on the day, and it can include clerical errors and mistakes, claim submission issues, or bad faith tactics.

How Long Do I Have to File a Claim and Get Paid?

Policyholders must review the insurance company’s guidelines and state laws regarding claims submissions. The rules depend on the type of claim, though most insurers require policyholders to submit a claim one year from the incident date.

How to Speed Up the Insurance Claims Process

Insurers have requirements policyholders must follow when submitting a claim, which can help claims get processed faster. This includes submitting accurate paperwork, providing thorough evidence, and cooperating with other insurer requests.

Policyholders can do everything right and find that the insurer denied their claim, and they have to appeal the decision. Things can happen outside the policyholder’s control, so it is wise to consider contacting a lawyer to avoid a lengthy claims fight.

What Can Delay My Claim Payment?

Policyholders who do not submit accurate paperwork or fail to comply with submission requirements are legitimate reasons an insurance company might deny a claim. Insurers might ask policyholders to correct errors or submit additional information to process the claim and get it back on track.

Claim denials also happen because bad faith insurers choose to stall a payout for unethical business reasons, and the process can drag on for weeks and sometimes months. You have a better chance of getting a bad faith insurer to reach a fair settlement with the help of an experienced attorney.

How To Dispute an Insurance Claim

Claim disputes are frustrating, especially when insurance companies hold up a claim for unethical reasons. It is best to be prepared when you dispute a claim; the following tips might help.

1. Be Aware of Bad Faith Insurance Practices

Bad faith insurance practices will likely catch you by surprise. Unethical insurers use various tactics to prevent a payout to line their pockets.

It is important to be mindful of unexplained things that do not make sense, such as agents avoiding communication with you, unexpected staff changes on your account, low settlement offers, or inappropriate investigation techniques.

2. Know Your Rights Under the Unfair Practices Act and the Fair Claims Settlement Practices Regulations

Laws and regulations exist so insurance companies do not take advantage of policyholders. Some states are better than others at enforcing these laws, but it is always important to have your own back and understand what to do if you are experiencing unfair claims practices.

3. Talk to the Claims Manager

Sometimes, insurance companies ask that their agents make the claims process difficult. In other cases, an agent might not resolve your claim for several reasons. You can escalate the issue and speak with a Claims Manager if you feel your case is not progressing or there is questionable behavior.

4. Request an Internal and External Review

Intervention is often necessary when insurance companies fail to process legitimate claims. Internal reviews ask that the insurance company reconsider its primary claims decision, while third parties, through an external review, can offer an unbiased perspective that can override the insurer’s decision.

5. Consult an Insurance Dispute Attorney

When there is evidence of inappropriate pushback from your insurance company regarding an eligible claim, it might be time to consult an attorney so they can get to the bottom of it. The presence of a lawyer is sometimes enough to force an insurance company’s hand to settle the claim, and Wallace Law has years of experience successfully facing big insurers head-on.

We Can Fight Your Insurance Company for You

Unethical insurance companies might draw on a wide variety of ploys to claim delays or denials. At that point, policyholders have a weighty choice to make. They can continue to fight the claim, settle for less money than they deserve, or drop the claim altogether.

It is not necessary to give up and it is not necessary to go it alone. There are options on the table.

Wallace Law is a go-to insurance dispute firm, and we work for the people — the frustrated policyholders that greedy insurers take advantage of every day. Good people lose time and money during claim disputes, but this does not have to be your reality, and we want to make sure of that.

We go after bad faith insurers that practice unethical claims procedures so you can get the money you deserve from your insurance policy. Contact Wallace Law today for a free legal consultation from the experts who know every trick in the book — and how to beat them.